TBS’ stake in Tokyo Electron (TEL) cannot be rationalised as a means of strengthening a business relationship between the two companies, as no such relationship exists. As we understand it, TBS’ business ties with TEL are limited to a capital infusion conducted 54 years ago and TEL’s occupancy of a TBS-owned building. A transaction that occurred more than half a century ago, and which has no bearing on the current performance of the company, is not an adequate justification for such a large shareholding. Nor is TEL’s occupancy of a TBS building.

TEL accounts for 19% of TBS’ assets and as such poses a large risk for shareholders and stakeholders. The quality of TEL’s business is not disputed, nor is TEL’s success and the positive impact it has had for all TBS shareholders. However, shareholders would have benefited to the same extent had they held shares in TEL themselves. The fairest, and most efficient, structure for shareholders to gain exposure to TEL is to own the shares directly. Thereafter shareholders can make an informed decision on the risk characteristics of TEL, appropriately evaluating whether they wish to bear such risk, and form their own conclusions on the merits of an investment in TEL.

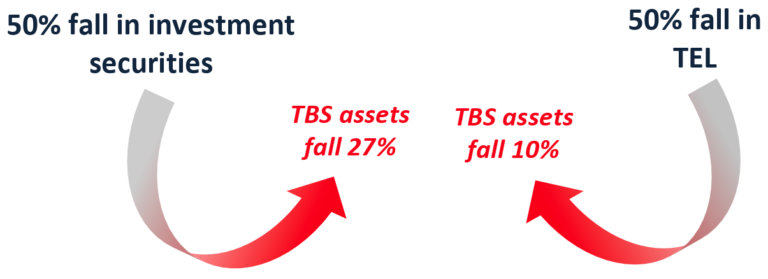

It is a flawed argument to suggest that TBS is not exposed to undue, and uncontrollable, risks from its investment securities. A 50% decline in TEL’s share price would see TBS’ assets fall by 10%. Such a decline for the entire investment securities portfolio would reduce TBS’ assets by 27%. TBS management can do nothing to mitigate this risk, as the erratic nature of stock markets is out of their control.

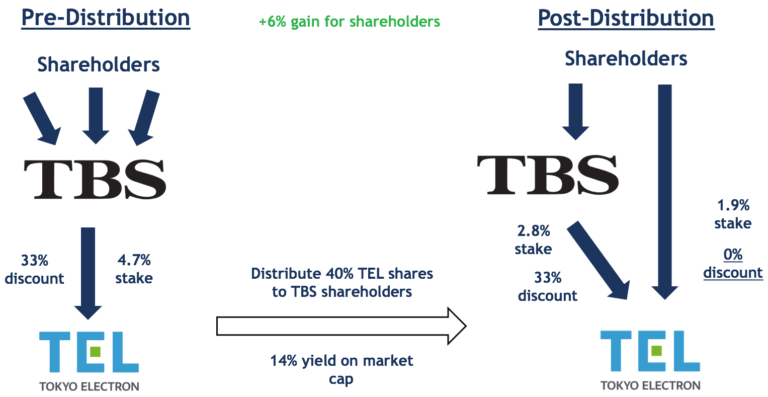

TBS shareholders should receive an uplift on the distributed TEL shares, to the extent that the market places a discount on their valuation when held by TBS. TBS trades on a 33% discount to our estimate of intrinsic value, and, by definition, shares removed from this structure would have a no discount. While the gain is short-term, the narrower discount that TBS should trade on is permanent and should increase TBS’ corporate value over the long-term.

The distribution of TEL shares is a first step in the reduction of TBS’ discount, and in no way would such a small distribution damage TBS’ capital strength. The modesty of this partial distribution is highlighted when comparing TBS’ post-distribution balance sheet to its peers, and to its current standing.

This website, and the information contained herein, (collectively referred to as “the Website”) is being provided for the shareholders of Tokyo Broadcasting Holdings. Inc. (“TBS”) for information purposes only. Asset Value Investors Limited (“AVI”) is the investment manager of one of the shareholders of TBS, namely British Empire Trust plc (“BTEM”).

AVI is authorised and regulated by the UK Financial Conduct Authority (“FCA”) and is also registered as an Investment Advisor with the United States Securities and Exchange Commission (the “SEC”) under the United States Investment Advisors Act of 1940.

The Website is directed only at Professional Clients or Eligible Counterparties as defined by the UK FCA.

AVI sent a written proposal addressed to TBS (the “Proposal”) through which AVI seeks to ask shareholders to vote on a distribution of in-kind shares or cash. The Proposal is accessible through the Website. AVI created the Website to help enable visitors to reach their own conclusion regarding whether or not to support the Proposal.

The Website was created solely for the purpose mentioned above and is provided for information purposes only. AVI is by no means soliciting or requesting other shareholders of TBS to jointly exercise their shareholders’ rights with AVI (including, but not limited to, voting rights).

AVI declares that it does not intend to be treated or deemed a “joint holder” (kyo-do hoyu-sha) with other TBS shareholders under the Japanese Financial Instruments and Exchange Act by virtue of disseminating information through the Website or engaging in dialogue with other TBS shareholders in or through this Website.

The Website exclusively represents the opinions, interpretations and estimates of AVI in relation to TBS’s business and governance structure. AVI is expressing such opinions, interpretations and estimates solely in its capacity as an investment manager to BTEM.

The information contained herein is derived from proprietary and non-proprietary sources deemed by AVI to be reliable. While AVI believes that reasonable efforts have been made to ensure the accuracy of the information contained in the Website, AVI makes no representation or warranty, expressed or implied, as to the accuracy, completeness or reliability of such information.

本ウェブサイトならびにここに含まれるすべての情報(以下、総称して「本ウェブサイト」といいます)は、株式会社東京放送ホールディングス(以下、「TBS」)の株主のために情報を提供するという唯一の目的で開設しております。アセットバリューインベスターズ(以下、「AVI」)は、TBSの株主であるブリティッシュ・エンパイア・セキュリティーズ・アンド・ジェネラル・トラスト・ピーエルシー(「BTEM」)の資産運用管理者です。

AVIは英国の金融行為監督機構(「FCA」)の認可および規制を受けており、また米国1940年投資顧問法に基づき投資顧問として米国証券取引委員会(「SEC」)に登録しております。

本ウェブサイトは、英国FCAが定めるプロ顧客ならびに適格取引先のみを対象としています。

AVIはTBSに対して、現物配当または現金配当を行うことについて株主総会決議を求める提案書(以下「本提案」)を送付しました。本提案は本ウェブサイトより入手できます。AVIは本ウェブサイトを閲覧される皆さまが本提案を支持するか否かについて、ご自身で判断される際にお役に立てればと考え、本ウェブサイトを開設しました。

本ウェブサイトは、上記の目的のためだけに開設されたものであり、情報の提供のみを目的として掲載しております。AVIは、TBSの他の株主の皆さまに対してAVIと共同で株主権(議決権を含みますがそれに限りません)を行使していただきたいと依頼、または要請しているわけではありません。

AVIは、本ウェブサイトを通じての情報提供又は本ウェブサイトを通じて他のTBS株主と対話を行うことにより、他の株主と金融商品取引法の上の「共同保有者」として扱われ、またはみなされることを意図しておりません。

本ウェブサイトは、TBSの事業およびガバナンス体制に関するAVIの見解、解釈 、評価を掲載したものであり、AVIはあくまでBTEMの資産運用管理者の立場からこれらの見解、解釈 、評価を述べております。

本ウェブサイトに掲載される情報は、AVIが信頼できると判断した専有又は非専有の情報源から得たものです。AVIは本ウェブサイトに掲載する情報の正確性を確保するために合理的な注意を払っておりますが、その正確性、完全性および 信頼性について明示・黙示にかかわらず一切の表明・保証をするものではありません。