ROSS MCGARRY of Asset Value Investors explores the investment opportunity we are seeing in Korea.

Executive Summary

The KOSPI has achieved a remarkable re-rating in 2026, reaching a new all-time high above 8,000 and returning +29% in May alone. Yet beneath the headline figures lies a tale of two markets. Samsung Electronics and SK Hynix now account for c. 53% of the KOSPI index and have driven the overwhelming bulk of this year’s gains. Strip them out, and the rest of the market returned just +5% in May versus +29% for the headline index. The Korea Discount has not been erased; it has been obscured by one of the most dramatic earnings inflections in global equity market history.

For bottom-up investors, this bifurcation represents an opportunity. Two-thirds of all KOSPI-listed companies still trade below book value, with 41% below 0.5x. Across AVI’s investable universe of over 600 names, the average price-to-book stands at c. 0.6x, yet the top 100 companies by quality metrics display average EBIT margins of 17%, three-year EBIT CAGRs of +14%, and ROICs of 12%. Beyond memory and beyond the index, the value is still there.

The case for unlocking it has also never been stronger. Unprecedented political alignment, a tightening regulatory framework – including the upcoming anti-stock price suppression act and stewardship code revisions – as well as materially stronger minority shareholder protections have shifted the balance of power in ways that make activist engagement in Korea increasingly effective.

This paper argues that the breadth of opportunity in Korean equities remains as compelling as ever, and that the next leg of performance will require, and is increasingly likely to receive, a more decisive push from government on corporate governance reform.

I. The Memory Super-Cycle: Earnings Inflection of Historic Proportions

An Earnings Inflection of Historic Proportions

The semiconductor industry has historically been a deeply cyclical one. The vicissitudes and resulting mergers and bankruptcies have taken the world from c.30 DRAM players to just three today: Samsung Electronics, SK Hynix and Micron.

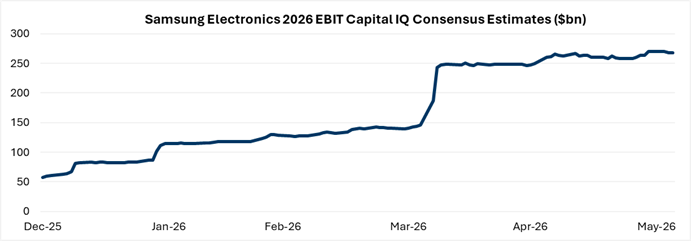

Against this constrained supply the advent of AI has sent demand parabolic, with a memory super-cycle, driven by accelerating High Bandwidth Memory (“HBM”) demand, pushing memory prices higher. One metric which illustrates the immense magnitude of this earnings inflection is the upward revisions to Samsung’s 2026 consensus EBIT, where the sell-side had initially been modelling c. +137% YoY growth at the start of 2026, but have since been revised up to c.+700% YoY. In $ terms, expectations for EBIT in 2026 have gone from $72bn to $230bn – and that’s even after recent labour negotiations have resulted in an average $400k profit bonus per employee. On current estimates, Samsung is on track to become the second most profitable company on earth in 2027, behind only NVIDIA.

Source: Capital IQ[1]

Goldman Sachs paints an equally striking picture at the index level: consensus has revised 2026 earnings from +48% at the start of the year to +277% currently. Even stripping out Samsung Electronics and SK Hynix, the rest of the market is now expected to grow 2026 profits by +57%, up from +20% in January – a reminder that the earnings upgrade cycle, while concentrated, is broader than many appreciate. Specific sectors such as capital goods (+22% NP revision), IT appliances (+179%), shipbuilding (+18%), transportation (+59%), and health care (+18%) are all showing meaningful growth profiles.

Source: Goldman Sachs Investment Research

Index Concentration, Valuation and the Trillion Dollar Question

Samsung Electronics and SK Hynix now represent approximately 52% of the KOSPI, with market caps of c. $1.5tr and $1.1tr respectively.

Source: FactSet

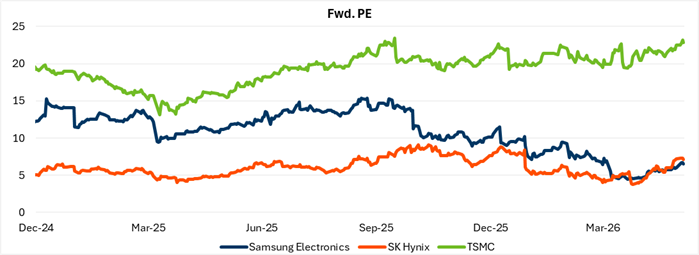

On a trailing price-to-book basis, Samsung Electronics trades at c. 5x book and SK Hynix at c. 10x — both at record levels and well above prior cycle peaks.

Source: Capital IQ

The market is increasingly convinced that this memory upcycle may prove more durable than previous ones. Supply-demand analysis points to persistent DRAM and NAND undersupply extending through at least 2028. This leverage has in turn led to binding long-term agreements (“LTAs”) across the sector, where rather than just being volume-based, contracts have embedded fixed price protections, enhancing earnings visibility, reducing cyclicality and improving through cycle returns on capital. In turn investors are debating whether these developments warrant such companies to be valued on an earnings basis – as opposed to a price to book basis. At c. 6x 2026e PE there is certainly room for SEC to continue to re-rate, particularly as investors appreciate the advancements the company has made in HBM.

Source: Capital IQ

That said, we do not believe the leopard can entirely change its spots. The industry remains cyclical and prone to great booms and busts and even with improved LTA contracts the current super cycle will at some point turn. Calling when this will be is of course the billion (trillion!?) dollar question and one the many market participants are trying to figure out.

Source: Goldman Sachs Global Investment Research, Company data

The recent emergence of Chinese domestic memory producers also represents a latent but growing tail risk to the durability of the current upcycle. ChangXin Memory Technologies (CXMT), China’s leading DRAM producer, has expanded rapidly from a low base, capturing an estimated 7–8% of the global DRAM market in early 2026.

In NAND flash, Yangtze Memory Technologies (YMTC) has similarly accelerated, accounting for approximately 13% of global NAND output in Q1 2026, on par with SanDisk and Kioxia. Both companies have pending IPOs to capitalise on the AI capex boom and raise capital that will, in turn, fund further capacity expansion.

The more nuanced emerging risk is therefore not whether the Chinese players flood the HBM market, where CXMT lags by an estimated three to five years and YMTC has yet to produce a single commercial DRAM die, but rather that Chinese producers flood the commodity DRAM and NAND segments, compressing average selling prices and, in turn, the supernormal profits of the major memory players.

II. The Market Beneath the Surface: Persistent Undervaluation

Market Breadth: A Bifurcated Landscape

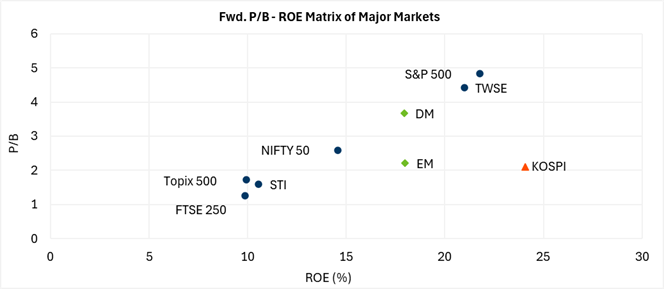

The KOSPI’s headline price-to-book now stands at 2.5x, in-line with the EM average. This is a remarkable achievement in just over twelve months, having re-rated from 0.9x in December 2024.

Source: CLSA

However, this flatters the breadth of the re-rating, with two thirds of all companies on the KOSPI still trading below book value and 41% below 0.5x. This is significantly higher than in equivalent markets such as Japan, the USA, or Europe.

Source: AVI, Capital IQ

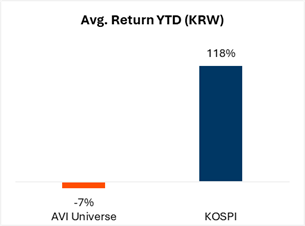

The same can be said of the index performance, as since election day in June 2025, the KOSPI has returned +266% on a headline basis, but only +97% on an equal-weighted basis. Year to date, the KOSPI has returned +118%, while the equal-weighted KOSPI has returned +49%. In May specifically, the KOSPI returned +35%, but the equal-weighted KOSPI returned just +6%. A vast difference in performance which has only been widening. The headline index performance obfuscates the abundance of value on offer in the Korean market for bottom-up investors.

Source: MSCI

The AVI Universe: Left Behind, Over-capitalised and Undervalued

Within the Korean market, the evidence of this is striking.

AVI is screening all 2,300 non-financial listed companies, applying both a liquidity and capitalisation threshold. This leaves us with an investable universe of over 600 names.

Across this universe of names, the average price-to-book ratio stands at c. 0.65x, with an average asset-backing to market cap ratio of 130%, implying that the embedded value of underlying assets remains dramatically larger than the price being paid by the market. There also remains further hidden value on offer for bottom-up investors in the form of non-core real-estate holdings, with numerous companies owning significant portfolios of investment properties on their balance sheets, which are notoriously hard to screen for. Notably, 82% of our universe of names remains uncovered, even more than the KOSPI, creating a rich, undiscovered opportunity set.

Source: AVI, Capital IQ

Yet this undervaluation is not coming at the expense of quality, with the top 100 companies in our universe ranked by quality metrics (EBIT margins, earnings growth, ROIC, etc.) displaying average EBIT margins of 17%, 3Y EBIT CAGRs of +14%, and returns on capital of 12%.

Despite this underlying business quality, our universe of names has generated a median total return of -7% YTD (local) versus the KOSPI’s return of +118% and have barely participated in the re-rating story since it began last year.

Source: AVI, Capital IQ

We also note that the types of companies for which we are screening are also at the centre of the government’s focus for future structural reform – holding company discounts, treasury share cancellation, excess capital, dual-listings, low PBRs, and low payout ratios. All told, our universe is unloved, undervalued, and under-researched, with the valuations of names not reflecting the underlying business quality, and with significant asset backing which makes them ripe for engagement.

AVI’s Korean Portfolio

Across AVI’s current Korean look-through holdings, the picture is similar. Our current portfolio of names has generated an average total return of +46% since we started investing into Korea last year, contributing c. +6% to AGT’s NAV over that time. However, the names linked to the AI/memory trade are responsible for 108% of this contribution, meaning effectively all non-AI/memory names have been detractors from our returns over the last twelve months, in-line with the experience of our wider universe.

| % Returns since 12-Jun-25 | Total Return (local) | Contrib. To Return (GBP) |

| Samsung C&T | 158.7 | 3.7 |

| Hyosung Corporation | 129.4 | 1.5 |

| HD Hyundai | 123.5 | 1.2 |

| All Non-AI Names | – | -0.5 |

| Total | – | 5.9 |

Source: FactSet, return period from 12-Jun-25 to 31-May-26

This portfolio continues to remain undervalued with the weighted average discount of the Korean companies we own standing at -55%, having slightly widened since the start of the year, and significantly wider than the AVI Global Trust’s portfolio average of -40%.

| Portfolio Company | Disc. 09-Jun-26 |

| Amorepacific Holdings | -53.3% |

| Cuckoo Holdings | -59.9% |

| Cuckoo Homesys | -48.0% |

| Daou Technology | -65.4% |

| GABIA | -44.6% |

| HD Hyundai | -38.1% |

| Hyosung Corp | -74.1% |

| Samsung C&T | -53.6% |

| Youngone Holdings | -40.7% |

| Weighted Avg. Discount | -55.3% |

Source: AVI estimates

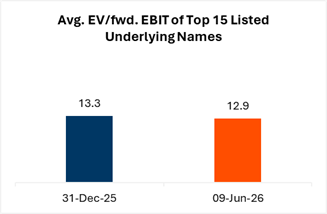

The underlying quality of our portfolio names remains high, however, with expected average 3Y revenue and EBIT growth of +9% and +17% respectively, average OP margins of 23% and a trailing ROE of 21% (all simple average and excl. Samsung Electronics). Despite their strong financial profile, our underlying portfolio has in fact become cheaper year to date, as their earnings continue to be revised up.

During May, we visited South Korea, marking our fifth visit to the country in the past couple of years. We spent the week meeting with the management of our portfolio companies to discuss private engagement materials we had sent them, as well as meeting with like-minded domestic activists to exchange ideas. Although the larger cap AI/memory names have been star performers to date, we expect that the most exciting long-term opportunities will be the smaller-cap laggard names where there is extreme overcapitalisation and a genuine opportunity to engage with management to unlock this value.

We continue to believe that the opportunity in Korean equities is as exciting as it has been at any point in our time following this market, and that more can, and needs, to be done to sustainably drive a re-rating across all companies.

III. The Activism Opportunity

The Case for Activist Engagement in South Korea

The Korea Discount is an institutional feature of the Korean market, embedded in decades of chaebol-centric capital allocation, cross-shareholding structures, and a historically weak tradition of minority shareholder engagement. However, the case for activism in South Korean equities has strengthened materially over the past year. Three factors stand out:

First, there is unprecedented political alignment. Unlike previous reform cycles that stalled in implementation, the current Value-Up programme has the backing of a government with a super-majority in the National Assembly, giving the DPK a legislative runway until the next general election in 2028. President Lee’s approval rating stands at c. 60% and the DPK won in a landslide victory in Korea’s June 2026 regional elections, the first major electoral test since his government began in June 2025 – suggesting that this supermajority may continue until the next Presidential election in 2030.

Second, the regulatory framework is becoming more prescriptive, far beyond the initial Value Up plan disclosure suggestions of the previous government. The policy roadmap for 2026 is a comprehensive agenda spanning stewardship code revisions, expanded capital market act amendments (including mandatory tender offer rules that would ensure minority shareholders receive control premiums), and the Anti-stock price suppression act (explained later) — all of which would further tighten the governance framework within which companies must operate and their incentives to act in the interest of minority shareholders.

Third, minority shareholders are now much more protected and have stronger voting rights, with the balance of power having shifted more in their favour than at any other point in Korean market history. More specifically, the three rounds of Commercial Act amendments passed since mid-2025 have laid the groundwork for activist investors to be able to start engaging with controlling shareholders.

Directors are now legally required to act in the interests of all shareholders; the 3% voting cap in audit committee elections has been tightened; cumulative voting is now mandatory for large listed companies; and most consequentially, all existing treasury shares have been mandated to be cancelled within 18 months, and all new treasury shares within one year of acquisition, extinguishing one of the most widely-abused tools for entrenching control.

A short summary of the changes to date:

| Reform | Key Provision | Date Passed |

| Commercial Act – First Amendment | Directors’ fiduciary duty explicitly extended to all shareholders; mandatory electronic shareholder meeting; expansion of 3% voting rule to both internal and independent directors when electing audit committee members | July 2025 |

| Commercial Act – Second Amendment | Mandatory cumulative voting introduced; expansion of election for audit committee members from one member to two or more members | August 2025 |

| Dividend Tax Reform | Dividend income separated from ordinary income tax. For corporates with high payout ratios (>40%) or with large dividend increases (+5% YoY) and above 25% payout ratio, separate taxation of dividends at 30% (vs. 49% currently) | November 2025 |

| Commercial Act – Third Amendment | Mandatory treasury shares acquired after March 2026 must be cancelled within one year of acquisition, all existing within 18 months | March 2026 |

Source: National Assembly, FSS

What More The Government Can Do

Yet it would be naive to assume that regulatory change alone will be sufficient. Many controlling shareholders are actively resisting reform. Over the last twelve months, we have seen companies rushing subsidiary listings through before they are outlawed; treasury shares being tied up in complex transactions to circumvent the cancellation deadline; cash-rich companies buying non-core real estate to pre-empt pressure to return capital to shareholders; articles of association being amended to make it harder for minorities to propose or appoint directors; and AGM notices being kept artificially short to foreclose shareholder proposals entirely. Turning to Value-Up statements, many amount to little more than vague boilerplate commitments for growing profitability.

There remains a lot to do, but, encouragingly, reform momentum remains strong. Although the corporate governance agenda remains a work in progress, the below table offers a rough guide for changes expected in 2026:

| Policy Area | Key Provision |

| Anti-stock price suppression | Extend the unlisted company inheritance tax calculation methodology to listed companies trading below 0.8x PBR, using weighted blend of adjusted NAV and net income, with a protective floor at 80% of NAV |

| Mandatory tender offer | Acquirer required to offer to purchase up to 100% stake to ensure minority shareholders can exit at the same premium as majority owner |

| Capital allocation & Corporate Governance Disclosure | Expansion to all KOSPI companies; disclosure of shareholder return vs. cost of capital using ROE and ROIC |

| Stewardship code revisions | Private committee-led implementation monitoring, and Stewardship Code compliance assessments incorporated into NPS asset manager selection |

| Dual listing regulations | Tightening guidelines to clarify definitions and approval criteria |

Source: National Assembly, Local Media, Goldman Sachs Global Investment Research

Beyond the current agenda, AVI has identified several additional steps which would help to drive a broad-based re-rating:

Stronger NPS engagement: The National Pension Service, with c. KRW1,100tn of assets, is one of the most powerful potential catalysts for governance improvement. It was disappointing to see them side with controlling shareholders at this years’ AGMs, and they must be willing to side with activist shareholders in the future if real change is to occur.

Enhanced Value-Up disclosure requirements: The current framework focuses on companies trading below book value. This should be extended to holding company discounts, companies with discounted preferred stock in issue, and those carrying net cash, investment securities, and non-core real estate surplus to operating needs.

Preferred share convergence: Korea’s dual share structure, in which preferred shares typically trade at discounts of 30–50% to ordinary shares despite carrying equivalent economic rights, represents a persistent and unnecessary value destruction mechanism. We call on the regulator to push companies to eliminate or converge the two classes of shares

Mandatory simplification of cross-shareholding structures: Korea’s web of intra-group shareholdings remains among the most complex in any major market, creating circular ownership arrangements which systematically disadvantage minority shareholders, due to the opaque governance structures they create. Time-bound unwinding requirements would unlock substantial value across the market and reduce the information asymmetry between controlling and minority shareholders.

IMPORTANT INFORMATION

This document is issued by Asset Value Investors Limited (“AVI”) which is authorised and regulated by the Financial Conduct Authority (UK). The distribution of this document may be restricted by law and persons into whose possession it comes are required to inform themselves of and comply with any such restrictions. The information in this document is selective and subject to verification, completion and amendments. As such, all information and research material provided herein is subject to change and this document does not purport to provide a complete description of the investments or markets referred to or the performance thereof. No undertaking, representation, warranty or other assurance, express or implied, is or will be made and no responsibility or liability is or will be accepted by or on behalf of AVI or by any of their respective officers, servants or agents (as applicable) or by any other person as to or in relation to the accuracy or completeness of this document or the information or opinions contained herein and no responsibility or liability is accepted by any of them for the accuracy or sufficiency of any such information. All opinions expressed in this document are subject to change without notice and do not constitute advice and should not be relied upon. The contents of this document are not intended to constitute, and should not be construed as, investment advice. Past performance is not a reliable indicator of future results and you may not get back the full amount invested.

Scan to visit our Insights page:

[1] Note: all pricing data as at 31/05/2026

The content of this website is issued by Asset Value Investors Limited (“AVI”), 2 Cavendish Square, London W1G 0PU. AVI is authorised and regulated by the Financial Conduct Authority of the United Kingdom (the “FCA”) and is a registered investment adviser with the Securities and Exchange Commission of the United States. While the Investment Manager is registered with the SEC as an investment adviser, it does not comply with the Advisers Act with regard to its non-U.S. clients.

To the extent that material on this website is issued in the UK, it is issued for the purposes of the Financial Services and Markets Act 2000

Intended Audience

The information on this website is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced on this website. The information contained on this website is subject to change without notice.

It is your responsibility to observe all applicable laws and regulations of any relevant jurisdiction.

This website is primarily intended for United Kingdom (“UK”) residents. It is not intended for distribution to, or use by, any U.S. persons or persons in any other country where such distribution, publication or use would be contrary to local law or regulation or in which AVI does not hold any necessary licence or registration. Individuals or entities in respect of whom such prohibitions apply, must not access or use the AVI website.

No Tax or Legal Advice

Nothing on this website constitutes investment, legal, tax or other advice nor should it be relied upon in making an investment decision.

Money Laundering

As a result of money laundering regulations, additional documentation for identification purposes may be required when you make your investment. Full details are contained in the relevant subscription documents.

Investment Decisions

As with all financial or investment matters, you should exercise great care in using the information provided on this website or available through links from this website. You should research the facts, opinions and strategies mentioned in this website before making any financial investment decisions. If you are unsure about the meaning of any information provided, please consult your financial adviser or other professional adviser.

No Warranty; Limitation on Liability

Neither AVI, any of its directors, officers or employees, nor any third party vendor, will be liable or have any responsibility of any kind for any loss or damage that you incur in the event of any failure or interruption of this site, or resulting from the act or omission of any other party involved in making this site or the data contained therein available to you, or from any other cause relating to your access to, inability to access, or use of the site or these materials, whether or not the circumstances giving rise to such cause may have been within the control of AVI, or of any vendor providing software or services support.

All information and content on this website is subject to applicable statutes and regulations, furnished “as is”, without warranty of any kind, express or implied, including but not limited to implied warranties of merchantability, fitness for a particular purpose or non-infringement. We make no warranty as to the operation, functionality or availability of this website, that the website will be error-free or that defects will be corrected.

In no event shall AVI be liable to any indirect, incidental, special or consequential damages arising out of or in connection with the use of this website, the inability to use this site or any products or services obtained or stored in or from this website, whether based on contract, tort, strict liability or otherwise. These limitations also apply to any third-party claims against users.

Intellectual Property

Everything on this website is the valuable intellectual property of Asset Value Investors Limited, or their respective suppliers. We protect our intellectual property rights to the full extent of the law.

Copyright Policy

No permission is granted to copy, distribute, modify, post or frame any text, graphics, video, audio, software code, or user interface design or logos.

Hyperlinks

The existence of hyperlinks should not be construed as an endorsement, approval or verification by AVI of any content available on third party sites. By providing access to other websites, we are not recommending the purchase or sale of products or services provided by the website’s sponsoring organization. We do not review any of these third-party sites. AVI reserves the right to require written consent for, or request the removal of, any links to our website.

AVI disclaims all responsibility and liability for the content on third party sites.

Security

For your protection, we require the use of encryption technologies for certain types of communications conducted through this website. While we provide those technologies and use other reasonable precautions to protect confidential information and provide suitable security, we do not guarantee or warrant that information transmitted through the Internet is secure, or that such transmissions will be free from delay, interruption, interception or error. You acknowledge and agree that users of this website and users, owners, or managers of third party websites may not: (i) collect or store personal data about other users of this website or (ii) upload, e-mail or otherwise transmit any material that contains viruses or any other computer code, files or programs that might interrupt, limit or interfere with the functionality of any computer software, hardware, database or file, or communications equipment that is owned, leased or used by AVI.

Privacy Policy

We encourage you to read AVI’s Privacy Policy which can be obtained by clicking the Privacy Policy button found on the Homepage.

General Terms

Deliberate misuse of any element of this website including, without limitation, hacking, introduction of viruses or similar code, disruption or excessive use or any use in contravention of applicable law, is expressly prohibited and we reserve the right to terminate your access to the website, and at our discretion, pass information to the legal authorities.

We reserve the right at any time on giving notice to change or modify these terms and conditions or to impose new conditions in respect of this website or to change or discontinue any aspect or feature of this website. We shall be entitled to terminate your access to this website at any time on giving notice to you and in any event if you commit any breach of these terms and conditions.

We shall have no liability to you for such termination. Notices may be served by any reasonable method including posting on this website.

You shall indemnify us from and against all actions, claims, proceedings, costs and damages (including any damages or compensation paid by us on the advice of its legal advisors to compromise or settle any claim) and all legal costs or expenses arising out of your use of this website, any breach of any applicable law, statute, ordinance, regulation or third party rights and any breach by you of the software licenses and service agreements governing the software made available to you in connection with this website.

These terms and conditions shall be governed by and construed in accordance with the laws of England without regard to conflicts of law principles. Nothing in these Terms and Conditions will exclude or restrict any duty or liability we may have under applicable rules or regulations.

The content of this website is issued by Asset Value Investors Limited (“AVI”), 2 Cavendish Square, London W1G 0PU.

AVI is authorised and regulated by the Financial Conduct Authority of the United Kingdom (the “FCA”) and is a registered investment adviser with the Securities and Exchange Commission of the United States. While the Investment Manager is registered with the SEC as an investment adviser, it does not comply with the Advisers Act with regard to its non-U.S. clients.

Intended Audience

The information on this website is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced on this website. The information contained on this website is subject to change without notice.

This website is primarily intended for UK residents. It is not intended for distribution to, or use by, any U.S. persons or persons in any other country where such distribution or use would be contrary to local law or regulation.

It is your responsibility to observe all applicable laws and regulations of any relevant jurisdiction.

No Tax or Legal Advice

Nothing on this website constitutes investment, legal, tax or other advice nor should it be relied upon in making an investment decision.

Money Laundering

As a result of money laundering regulations, additional documentation for identification purposes may be required when you make your investment. Full details are contained in the relevant subscription documents.

Investment Decisions

As with all financial or investment matters, you should exercise great care in using the information provided on this website or available through links from this website. You should research the facts, opinions and strategies mentioned in this website before making any financial investment decisions. If you are unsure about the meaning of any information provided, please consult your financial adviser or other professional adviser.

No Warranty; Limitation on Liability

Whilst all reasonable care has been taken in the preparation of this website, AVI cannot guarantee the accuracy or completeness of such information, either expressly or implied. Neither AVI, any of its directors, officers or employees, nor any third party vendor, will be liable or have any responsibility of any kind for any loss or damage that you incur in the event of any failure or interruption of this site, or resulting from the act or omission of any other party involved in making this site or the data contained therein available to you, or from any other cause relating to your access to, inability to access, or use of the site or these materials, whether or not the circumstances giving rise to such cause may have been within the control of AVI, or of any vendor providing software or services support.

All information and content on this website is subject to applicable statutes and regulations, furnished “as is”, without warranty of any kind, express or implied, including but not limited to implied warranties of merchantability, fitness for a particular purpose or non-infringement. We make no warranty as to the operation, functionality or availability of this website, that the website will be error-free or that defects will be corrected.

In no event shall AVI be liable to any indirect, incidental, special or consequential damages arising out of or in connection with the use of this website, the inability to use this site or any products or services obtained or stored in or from this website, whether based on contract, tort, strict liability or otherwise. These limitations also apply to any third-party claims against users.

Intellectual Property

Everything on this website is the valuable intellectual property of Asset Value Investors Limited, or their respective suppliers. We protect our intellectual property rights to the full extent of the law.

Copyright Policy

No permission is granted to copy, distribute, modify, post or frame any text, graphics, video, audio, software code, or user interface design or logos.

Hyperlinks

The existence of hyperlinks should not be construed as an endorsement, approval or verification by AVI of any content available on third party sites. By providing access to other websites, we are not recommending the purchase or sale of products or services provided by the website’s sponsoring organization. We do not review any of these third-party sites. AVI reserves the right to require written consent for, or request the removal of, any links to our website.

AVI disclaims all responsibility for the content of third-party sites

Security

For your protection, we require the use of encryption technologies for certain types of communications conducted through this website. While we provide those technologies and use other reasonable precautions to protect confidential information and provide suitable security, we do not guarantee or warrant that information transmitted through the Internet is secure, or that such transmissions will be free from delay, interruption, interception or error.

You acknowledge and agree that users of this website and users, owners, or managers of third party websites may not: (i) collect or store personal data about other users of this website or (ii) upload, e-mail or otherwise transmit any material that contains viruses or any other computer code, files or programs that might interrupt, limit or interfere with the functionality of any computer software, hardware, database or file, or communications equipment that is owned, leased or used by AVI.

Privacy Policy

We encourage you to read AVI’s Privacy Policy which can be obtained by clicking the Privacy Policy button found on the Homepage.

General Terms

Deliberate misuse of any element of this website including, without limitation, hacking, introduction of viruses or similar code, disruption or excessive use or any use in contravention of applicable law, is expressly prohibited and we reserve the right to terminate your access to the website, and at our discretion, pass information to the legal authorities.

We reserve the right at any time on giving notice to change or modify these terms and conditions or to impose new conditions in respect of this website or to change or discontinue any aspect or feature of this website. We shall be entitled to terminate your access to this website at any time on giving notice to you and in any event if you commit any breach of these terms and conditions. We shall have no liability to you for such termination. Notices may be served by any reasonable method including posting on this website.

You shall indemnify us from and against all actions, claims, proceedings, costs and damages (including any damages or compensation paid by us on the advice of its legal advisors to compromise or settle any claim) and all legal costs or expenses arising out of your use of this website, any breach of any applicable law, statute, ordinance, regulation or third party rights and any breach by you of the software licenses and service agreements governing the software made available to you in connection with this website.

These terms and conditions shall be governed by and construed in accordance with the laws of England without regard to conflicts of law principles. Nothing in these Terms and Conditions will exclude or restrict any duty or liability we may have under applicable rules or regulations.

INVESTOR – Risk Warnings

It is very important that you read this warning and disclaimer before proceeding, as it explains certain legal and regulatory restrictions applicable to any investment services and products we provide.

The content of this website is issued by Asset Value Investors Ltd (“AVI”), 2 Cavendish Square, London W1G 0PU

AVI is authorised and regulated by the Financial Conduct Authority (“FCA”) in the United Kingdom.

This website is not directed at any person in any jurisdiction where it is illegal or unlawful to access and use such information. AVI disclaims all responsibility if you access any information in breach of any local law or regulation. All persons who access this website are required to inform themselves and to abide with all applicable local law, regulations and restrictions.

The information on this website is not directed at any person or entity in the United States, and this site is not intended for distribution or to be used by any person or entity in the United States unless those persons or entities are existing investors in funds managed by AVI and they have applicable US exemptions.

Nothing on this website constitutes investment, legal, tax or other advice nor should it be relied upon in making an investment decision.

The funds referred to in this website include: alternative investment funds (“AIFs”), UCITS funds, and a collective investment scheme registered in the Cayman Islands. The promotion of such funds and the distribution of offering materials in relation to such funds is accordingly restricted by law.

Shares in the funds mentioned in this website are not dealt in or on a recognised or designated investment exchange, nor is there a market maker in such shares, and it may therefore be difficult for an investor to dispose of his shares.

The information on this website is neither an offer to sell nor a solicitation of any offer to buy shares in any fund managed by AVI.

An application for shares in any of the funds referred to on this site should only be made having fully read the relevant prospectus and most recent financial statement and semi-annual financial statements published thereafter.

The Information is provided for information purposes only and on the basis that you make your own investment decisions and do not rely upon it.

AVI is not soliciting any action based on it and it does not constitute a personal recommendation or investment advice.

Should you have any queries about the investment funds referred to on this website, you should contact your financial adviser.

Past performance is not an indication of future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amount invested.

The funds noted in this website may be subject to higher risk and volatility than other funds and may not be suitable for all investors.

Exchange rates may cause the value of overseas investments and the income arising from them to rise or fall.

The levels and bases of and reliefs from taxation may change. Any tax reliefs referred to are those currently available and their value depends on the circumstances of the individual investor. Investors should consult their own tax adviser in order to understand any applicable tax consequences.

The information on this website, including any expression of opinion or forecast, has been obtained from, or is based on, sources believed by AVI to be reliable, but are not guaranteed as to their accuracy or completeness and should not be relied upon.

You should be aware that the Internet is not a completely reliable transmission medium. AVI does not accept any liability for any data transmission errors such as data loss or damage or alteration of any kind, including, but not limited to any direct, indirect or consequential damage, arising out of the use of the products or services referred to herein. This does not exclude or restrict any duty or liability that AVI has to its customers under the regulatory system in the United Kingdom.

To make a complaint about this website please send a written complaint for the attention of the Compliance Officer at the registered address: 2 Cavendish Square, London W1G 0PU.

You agree to indemnify, defend, and hold harmless AVI, its affiliates and licensors, and the officers, partners, employees, and agents of AVI and its affiliates and licensors, from and against any and all claims, liabilities, damages, losses, or expenses, including legal fees and costs, arising out of or in any way connected with your access to or use of this website and the Information.

The existence of hyperlinks should not be construed as an endorsement, approval or verification by AVI of any content available on third party websites. By providing access to other websites, we are not recommending the purchase or sale of products or services provided by the website’s sponsoring organization. We do not review any of these third-party websites.

No permission is granted to copy, distribute, modify, post or frame any text, graphics, video, audio, software code, or user interface design or logos.

Nothing on this site should be considered as granting any licence or right under any trademark of AVI or any third party.

Deliberate misuse of any element of this website including, without limitation, hacking, introduction of viruses or similar code, disruption or excessive use or any use in contravention of applicable law, is expressly prohibited and we reserve the right to terminate your access to the website, and at our discretion, pass information to the legal authorities.

We reserve the right at any time on giving notice to change or modify these terms and conditions or to impose new conditions in respect of this website or to change or discontinue any aspect or feature of this website. We shall be entitled to terminate your access to this website at any time on giving notice to you and in any event if you commit any breach of these terms and conditions. We shall have no liability to you for such termination. Notices may be served by any reasonable method including posting on this website.

These terms and conditions shall be governed by and construed in accordance with the laws of England without regard to conflicts of law principles. Nothing in these Terms and Conditions will exclude or restrict any duty or liability we may have under applicable rules or regulations. You irrevocably waive any right to a jury trial in any dispute or proceeding arising from the use of this site.